Farm Loan Calculator: How to Determine Payments for Agricultural Financing

Farm Loan Calculator: How to Determine Payments for Agricultural Financing

Farmers often need financing for land, equipment, or seasonal operations. Understanding the cost of borrowing is essential for making sound business decisions. A farm loan calculator helps estimate regular payments and total interest for agricultural loans. This guide explains how to use a farm loan calculator, what factors affect loan payments, and practical steps to calculate your farm loan payments with confidence.

What Is a Farm Loan Calculator?

A farm loan calculator is a digital tool that estimates payment amounts, interest costs, and repayment schedules for agricultural loans. This calculator uses basic loan information—such as the total loan amount, interest rate, and repayment term—to show how much you need to pay monthly or annually.

Farm loan calculators are available online or as downloadable apps. They are valuable for:

- Planning your cash flow

- Comparing loan offers

- Understanding long-term borrowing costs

According to the U.S. Department of Agriculture, nearly one out of every five U.S. farms uses a farm loan program each year. Using a calculator helps farmers prepare for these commitments.

Key Factors That Affect Farm Loan Payments

Several factors determine how much you pay on a farm loan. The main variables are:

- Loan Amount: The total money borrowed.

- Interest Rate: The cost of borrowing, shown as an annual percentage.

- Loan Term: How long you have to repay the loan (in years or months).

- Payment Frequency: How often you make payments (monthly, quarterly, or yearly).

- Type of Loan: Fixed-rate or variable-rate loans change payment calculations.

The interest rate is especially important. Even a small difference in rate can change your total repayment by thousands of dollars over time. According to Federal Reserve Economic Data, agricultural loan rates in the U.S. have ranged from 3% to over 8% in recent years.

Understanding these factors helps you use a farm loan calculator more effectively and choose the best loan for your needs.

How to Use a Farm Loan Calculator: Step-by-Step

Using a farm loan calculator is straightforward. Follow these steps to estimate your loan payments accurately.

- Collect Loan Details

Gather your loan amount, interest rate, loan term, and payment frequency. For example, if you borrow $200,000 at a 6% annual interest rate for 10 years, you will need these numbers to start. - Enter the Information

Input the data into the calculator’s fields. Most calculators have labeled boxes for each detail. - Choose the Payment Type

Select whether you want monthly, quarterly, or yearly payments. - View Results

The calculator will show:- Your regular payment amount

- Total interest paid

- Total loan cost (principal plus interest)

- Adjust for Comparison

Change interest rates, loan amounts, or terms to see how your payments change. This helps you compare different loan offers. - Record the Output

Save or print the payment schedule for your records.

Many agricultural lenders, including the Farm Credit Administration, provide online loan calculators for free. These tools are safe and do not require sensitive personal information.

Practical Example: Calculating a Farm Loan Payment

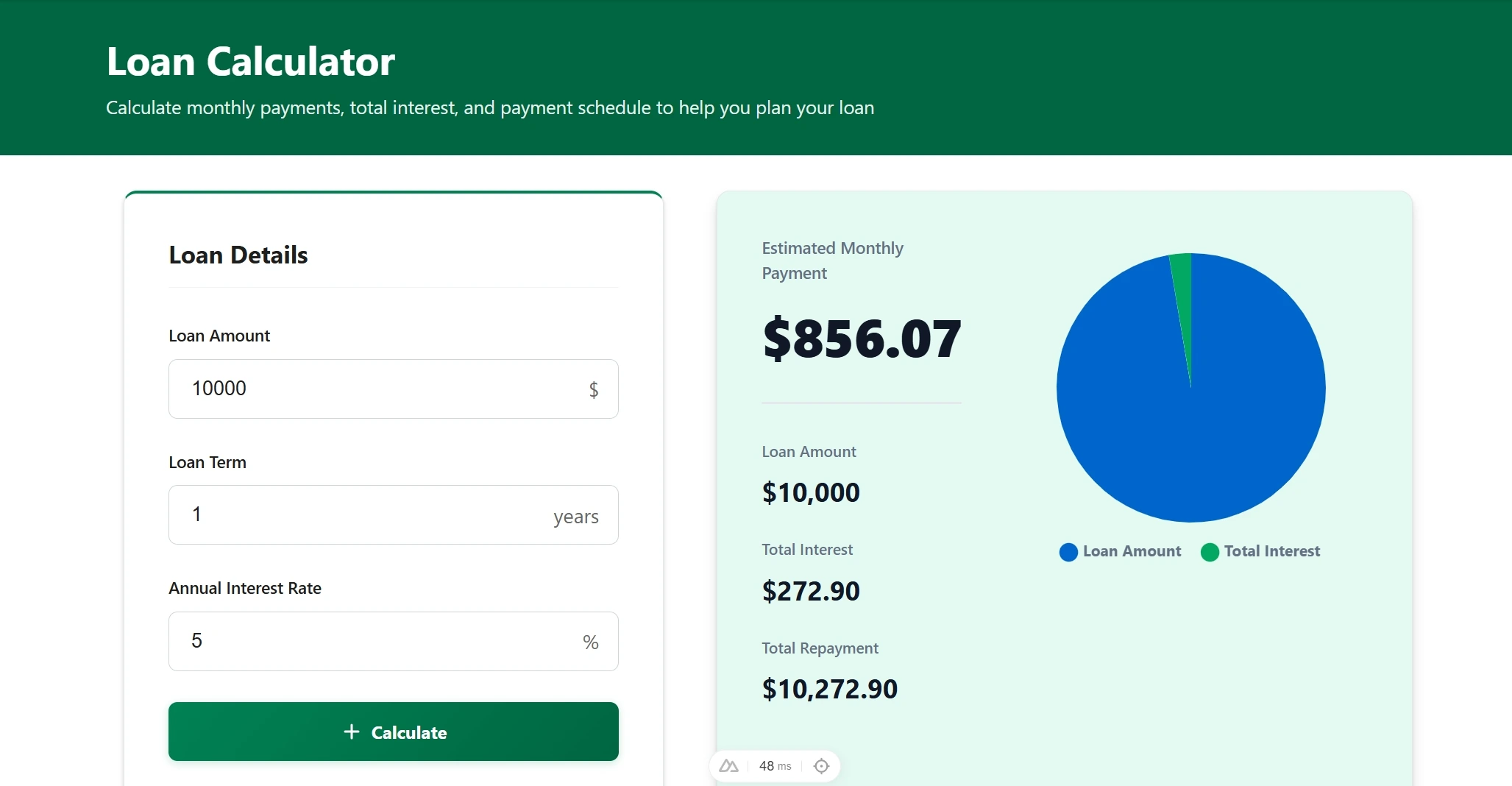

Suppose a farmer wants to buy equipment with a $150,000 loan. The lender offers a 5.5% fixed rate for 7 years, with payments due monthly.

- Loan Amount: $150,000

- Interest Rate: 5.5%

- Loan Term: 7 years (84 months)

- Payment Frequency: Monthly

When entered into a farm loan calculator, the monthly payment is about $2,147. Over the life of the loan, total interest paid is roughly $30,348. The total cost to repay the loan becomes $180,348.

This example shows how using a calculator helps you understand the true cost of borrowing. You can also see how longer loan terms reduce monthly payments but increase the total interest paid.

Why Use a Farm Loan Calculator Before Applying?

Using a farm loan calculator offers several advantages:

- Budget Planning: Know your payment obligations before signing a loan agreement.

- Interest Savings: Compare different loan products to find the lowest total cost.

- Informed Decisions: Avoid surprises by understanding how rates and terms affect payments.

- Negotiation Power: Use your calculated results to discuss better terms with lenders.

According to the National Agricultural Law Center, careful loan planning reduces the risk of financial strain and helps protect your farm’s long-term success.

Using these calculators is a best practice for all farmers considering agricultural financing. It supports better business decisions and financial health.